Three Debit Orders, Two Store Accounts, and a Credit Card Walk Into a Bar

That's not the start of a joke. That's the average South African's monthly repayment situation — and it's not funny at all.

I've been writing about personal finance in SA for the better part of a decade, and the pattern I see over and over is the same: someone takes a personal loan from Capitec for something reasonable. Then a Mr Price store account because the cashier made it sound painless. Then a credit card "just for emergencies" that somehow funds Uber Eats on a Tuesday. Before they know it, they're juggling five different payments on five different dates with five different interest rates — and they can't tell you the total amount they owe if you put a gun to their head.

That's where debt consolidation comes in. And before you roll your eyes — yes, I know, there are roughly 4,000 articles about this topic. But most of them are written by people who've never actually looked at what happens when you run the numbers with real South African interest rates, real lender products, and real NCR regulations. So let's do that.

What Consolidation Actually Is (in 30 Seconds)

You take one new loan. That loan pays off all your existing debts — the store accounts, the credit cards, the personal loans, whatever. Now instead of five payments, you have one. One debit order, one interest rate, one date to remember.

Simple concept. The devil, as always, is in the details.

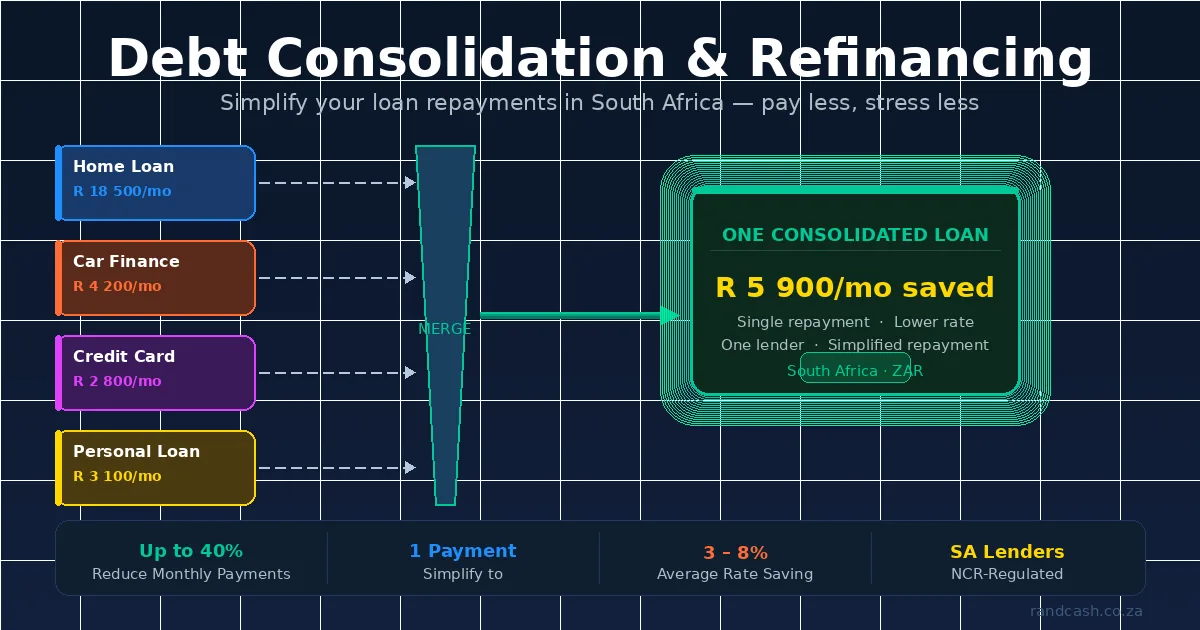

Let's Talk Numbers: A Real Scenario

Meet Thabo. He's not real, but his situation is — I've seen versions of it hundreds of times. Thabo earns R22,000 a month before tax in Johannesburg. Here's what he owes:

- Mr Price store account: R4,200 balance at 24% interest — monthly payment R380

- Woolworths card: R8,500 balance at 20.75% — monthly payment R620

- Capitec personal loan: R15,000 remaining at 18% over 24 months — monthly payment R1,180

- FNB credit card: R12,000 balance at 21.75% — monthly minimum R480

Total monthly payments: R2,660

Total debt: R39,700

Weighted average interest rate: roughly 20.4%

Now, Thabo applies for a consolidation loan. African Bank is currently offering consolidation loans starting from 11.75% p.a. for borrowers with good credit profiles. FNB's Credit Switch product goes up to R360,000 over 72 months. Nedbank offers up to R300,000.

Let's say Thabo gets approved at 16% — realistic for someone with a decent credit score and stable employment. He takes R40,000 over 36 months.

New single monthly payment: approximately R1,406

Monthly saving: R1,254

That's real money. That's groceries for two weeks. That's a chunk of rent in Soweto. That's breathing room.

But here's the catch nobody talks about

If Thabo had kept paying R2,660 across his original debts, most of them would've been cleared in 18-24 months. His new consolidation loan runs for 36 months. So yes, the monthly payment dropped — but he's paying for longer. The total interest paid over the life of the consolidation loan at 16% over 36 months comes to about R10,616. Had he muscled through the original payments, he'd have paid roughly R8,900 in total interest across all accounts.

He saved R1,254 a month in cash flow. He paid R1,716 more in total interest. Was it worth it? For most people — yes. Because the R1,254 monthly relief means they actually make the payments instead of missing them and getting defaults slapped on their credit report.

But you should know the trade-off exists.

The Refinancing Angle: Why 2026 Is a Decent Window

Here's something that makes this conversation more interesting right now than it was two years ago. The SARB has cut the repo rate six times since September 2024 — taking the prime lending rate from 11.75% down to 10.25%. That's 150 basis points of relief.

On March 26, 2026, the Reserve Bank held the rate steady for the second consecutive meeting, citing inflation risks from the Middle East situation. The market's now pricing in maybe one more cut this year, tops. So if you're sitting on older debt that was priced when prime was at 11.75%, you're essentially overpaying relative to what's available now.

This is where consolidation doubles as refinancing. You're not just simplifying your payments — you're replacing expensive old debt with cheaper new debt. A consolidation loan taken out today at prime + 6% gives you 16.25%. Two years ago, that same risk profile would've been prime + 6% = 17.75%. That 1.5% difference on R40,000 over 36 months saves you about R1,100 in total interest.

Not life-changing. But not nothing either.

Consolidation vs Debt Review: Know the Difference Before You Choose

This trips people up constantly. Debt counselling (also called debt review) and debt consolidation are not the same thing. Not even close.

Debt consolidation is just a loan. You apply, you qualify (or you don't), you get the money, your old debts get paid off. Your credit profile stays open — you can still apply for new credit. There's no legal process involved.

Debt review is a formal legal process under Section 86 of the National Credit Act. A registered debt counsellor declares you over-indebted, negotiates reduced payments with your creditors, and a court makes it official. While you're under debt review, you cannot take on new credit. Full stop. But — and this is the big upside — your creditors can't take legal action against you either. No garnishee orders, no repossession, no sheriff at your door.

The irony? The people who most need consolidation often can't get it because their credit is already shot. And the people who qualify for consolidation loans often don't need debt review yet. There's a gap in the middle where people fall through, and it's not great.

If you're already in arrears on multiple accounts and your credit score is below 600, consolidation probably isn't happening for you. Debt review might be the better path — and there's no shame in that.

What the Law Says You Should Know

The National Credit Regulator doesn't mess around. Every consolidation loan in South Africa falls under the NCA, which means:

Your lender must do a proper affordability assessment. They can't just hand you R40,000 because you asked nicely. If they lend to you and you clearly can't afford the repayments, that's reckless lending — and the agreement can be set aside by a court. This actually protects you, even though the assessment process feels annoying when you're sitting in the branch.

They must disclose the full APR before you sign anything. Not just the interest rate — the APR, which includes the initiation fee (capped at R1,207.50 + 10% of the amount above R1,000), the monthly service fee (capped at R69 per month), and credit life insurance if applicable.

And here's one people forget: the NCA gives you the right to settle early with a maximum penalty of three months' interest. So if you consolidate and then get a bonus or a better-paying job six months later, you can pay the whole thing off without getting hammered by penalties.

Draft amendments published in August 2025 (Government Gazette 53154) are tightening things further — particularly around how credit bureaus handle your data and how lenders must verify income. More protection for you, even if it means a slightly longer application process.

A Second Scenario: When Consolidation Goes Wrong

Meet Naledi. Also fictional, also painfully common. She consolidates R35,000 in debt into a single loan over 60 months to get the lowest possible monthly payment — about R850 a month at 18%.

Feels great. R850 instead of the R2,100 she was paying before. She's got breathing room.

Three months later, she's back at Edgars opening a new store account. "Just for the sale." Then a new credit card because the old one got paid off by the consolidation loan and the limit's just sitting there. By month twelve, she's got the consolidation loan plus R18,000 in new debt.

She's now worse off than before she consolidated. Way worse.

This is the number one risk with consolidation — and no amount of regulation can prevent it. The debt trap isn't the consolidation loan. It's the empty store accounts that whisper "use me" after consolidation pays them off.

The fix is brutal but simple: close the accounts. All of them. Cut the cards. Close the store accounts. If you can't trust yourself — and be honest here — ask the credit provider to close the facility entirely. Yes, your available credit will drop. Yes, your credit utilisation ratio might look weird temporarily. But it's better than being R53,000 in the hole.

Who Should Actually Consider This?

After covering this space for years, here's my honest take on who benefits from consolidation:

Good candidates:

- You have 3+ debts with different payment dates and you've missed at least one payment in the last 6 months purely from admin chaos — not because you can't afford it

- Your existing debts carry rates above 20% and you qualify for a consolidation rate below 18%

- You have the discipline to close old accounts after consolidation (or you'll get someone to hold you accountable)

- You've recently gotten a raise or changed jobs and your affordability profile has improved since you first took those debts

Bad candidates:

- You're already in arrears on multiple accounts — you probably won't qualify anyway

- Your total debt is under R10,000 — the initiation fees and service charges on the new loan eat too much of the savings

- You plan to extend the term to 72 months just to minimise the monthly payment without calculating the total cost of credit

- You haven't addressed why you got into this situation — consolidation treats the symptom, not the disease

How to Actually Do It

Right. Practical steps.

Step 1: Get your credit report. It's free once a year from each bureau — here's how to check your credit score for free. You need to know exactly what you owe and to whom.

Step 2: List every debt with its balance, interest rate, monthly payment, and remaining term. All of them. Even the Truworths card you forgot about.

Step 3: Compare consolidation loan offers from at least three lenders. Don't just walk into your bank and take whatever they offer. Use a comparison tool that pulls offers from multiple registered lenders at once — it takes a few minutes and gives you actual rates to compare.

Step 4: Calculate the total cost, not just the monthly payment. A loan at 16% over 36 months costs less in total than the same loan at 16% over 60 months, even though the monthly is higher. Use the total cost of credit figure that every lender must provide by law.

Step 5: If you consolidate — close the old accounts. I cannot stress this enough.

The Bottom Line

Debt consolidation isn't magic. It won't make your debt disappear. What it does — when used correctly — is turn a chaotic mess of payments into something manageable. One amount, one date, and often a lower interest rate than the average of what you're currently paying.

With prime sitting at 10.25% in March 2026 and rates the lowest they've been since early 2023, the window for consolidation-as-refinancing is genuinely decent. Personal loan delinquency in SA is at a staggering 53.4% right now. That tells me a lot of people are struggling with exactly this kind of payment chaos.

If that's you — don't sit on it until you start missing payments and your options narrow. Compare what's available, run the numbers yourself, and make a decision with your eyes open. Not because some article told you to "take control of your finances" — but because the maths either works in your favour or it doesn't. And now you know how to check.