Look, I know what you're thinking. Another budgeting article. You've probably heard this all before — the 50/30/20 rule, the spreadsheet talk, the "track every cent" lectures. But here's the thing: with inflation hovering around 3.5% and food prices up 12% since last year, budgeting isn't optional anymore in South Africa. It's survival.

The reality hitting South African households right now is brutal. A family of four now needs more than R4,000 just for basic groceries. Rent in a Johannesburg one-bedroom flat has jumped to R9,500. That's not a preachy statistic — that's your mate struggling to pay rent and groceries in the same month.

Why Your Current Budget Probably Isn't Working

Most people create a budget, stick to it for two weeks, then abandon it. Not because they lack discipline. It's because the budget doesn't match reality. You sit down with a spreadsheet, tell yourself you'll spend R300 on coffee for the month, and then life happens — a bakkie repair, load shedding damage, a kid's school fees due early.

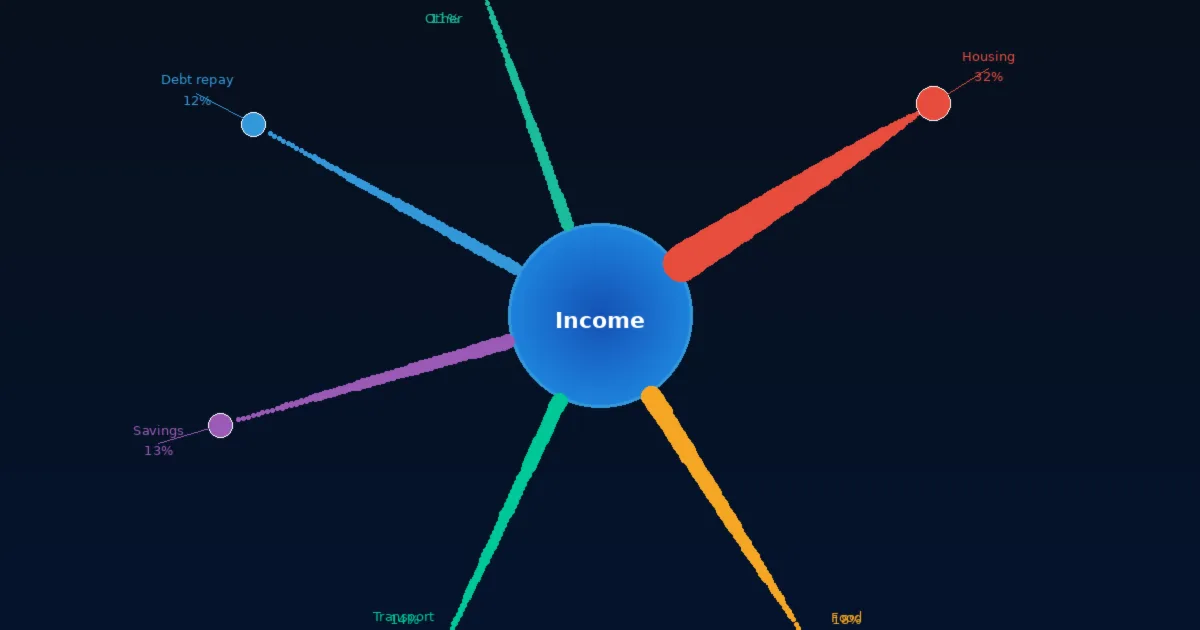

The real problem? The traditional 50/30/20 rule doesn't work for South Africans anymore. Sure, the logic is simple: 50% of after-tax income goes to needs (rent, food, transport, utilities), 30% to wants (entertainment, dining), and 20% to savings and debt repayment. But when housing and transport alone eat 60% of your salary, that framework falls apart.

I've seen people stress themselves sick trying to force their lives into a formula that was designed for a different country, a different economy, a different context entirely. That's not helpful.

The South African Reality Check

Let's be honest about what's eating your payslip right now. If you're living in a major metro, housing costs have surged 15% year-on-year. In Cape Town, a one-bedroom rental hits R13,000. Your electricity bill — which used to be a line item — is now a major expense. Eskom's tariffs have climbed over 11% for municipalities in the 2025/26 period, and that gets passed straight to households already stretched thin.

Then there's the debt piece. The average South African consumer carries R91,126 in debt — store accounts, personal loans, credit cards. The debt-to-income ratio nationally sits at 62.5%, meaning many households owe more than their annual take-home. That's not a number to ignore.

Add to this the fact that wage increases haven't kept pace with inflation, and you've got a genuinely difficult situation. Your salary increased 2% last year. Your rent increased 15%. The maths doesn't work.

Building a Budget That Matches Your Life

Forget the formula. Instead, start here.

Step 1: Know exactly what comes in. Write down your actual take-home salary. Not the gross figure your employer quotes — the amount you actually see in your bank account after tax, UIF, and medical aid. If you've got side income (freelance work, let's say), include that too. But only if it's reliable. Don't count on income that comes in maybe.

Step 2: Track what actually leaves. Not for a week. A full month. Pull your bank statements and go through them line by line. You'll be shocked. Most people don't realise how much they spend on subscriptions — Netflix, gym memberships they never use, insurance they've forgotten about. Get your phone bill, your electricity bill, your rent receipt. Write it down.

Step 3: Separate the non-negotiables. Housing. Food. Transport. Electricity. Insurance. These don't change month to month. Not easily, anyway. That's your floor — the amount you absolutely must spend to keep the lights on (metaphorically and literally). Calculate it exactly.

Step 4: Look at what's discretionary. Everything else — dining out, streaming services, hobbies, new clothes — is fair game. This is where you can actually cut. Not by being miserable, but by being intentional. Do you actually watch all those streaming services? Would you miss them? Probably not as much as you'd miss that extra R500 in your account at month's end.

Step 5: Build in chaos money. In South Africa, you need a buffer. A pothole that wrecks your tyre. A medical emergency. A family member asking to borrow money. If you don't budget for chaos, chaos will budget you. Put aside even R300 a month if that's all you can manage. It matters.

The Tools That Actually Work

You don't need fancy software. Seriously. A spreadsheet does the job. Google Sheets is free. So is Calc. Or grab a notebook and use a pen if that's more your speed. The tool doesn't matter. Consistency does.

If you want something that walks you through it, there are apps — plenty on the Google Play Store don't cost anything. Pick one that feels intuitive. The best budget app is the one you'll actually use, not the one that looked impressive in the App Store.

Some people swear by the debt snowball method. Others use the debt avalanche approach. The truth? Both work. What works is the method you stick with.

The Mistakes That Sink Budgets

Going too hard. You create a budget so strict that by day 10 you're exhausted. You can't eat out at all, can't buy anything new, can't spend money on anything vaguely nice. By day 15, you've abandoned the whole thing. Better to be realistic: allow yourself something small each month that brings joy. R100 for pizza night. Whatever. If your budget feels like punishment, you won't maintain it.

Never reviewing it. Life changes. Your rent increases. You get a new job. A kid is born. Your budget needs to evolve with you. Look at it every month. Are you overspending in a category? Can you adjust? Did your income increase? Reallocate. A budget is a living document, not something you set and forget.

Budgeting in a vacuum. If you're in debt review or carrying serious debt, budgeting alone won't fix it. You might need to consolidate your debts or explore other options. There's no shame in that. Better to face it than pretend the problem isn't there.

Ignoring your credit situation. If you've got multiple credit cards or store accounts, your budget isn't your real problem — your debt structure is. Check your credit report for free and understand what you're actually dealing with. Knowledge beats ignorance every time.

The Uncomfortable Truth About Budgets

A budget is just organisation. It doesn't create money that isn't there. If you're genuinely earning R12,000 a month and spending R14,000, no spreadsheet will fix that. You have three options: earn more, spend less, or get help with existing debt.

Some of these options are hard. Earning more means side hustles, renegotiating salary, or picking up extra work. Spending less means sacrifices — smaller flat, cheaper neighbourhood, fewer subscriptions. Getting help with debt means potentially talking to a debt counsellor or exploring consolidation loans to lower your monthly obligations.

None of these are quick fixes. But they're real fixes. A budget just makes sure you can see what you're working with.

Where to Start Tomorrow

Pull your last three bank statements tonight. Don't judge yourself. Just look at what's actually happening. Tomorrow, grab a piece of paper or open a Google Sheet. Write down your monthly income (actual, after-tax number). Write down your housing cost. Your transport. Food. Utilities. Go through your recent bank activity and find the number you're actually spending in each category.

That's your budget. Not a fantasy budget. Not a budget you're going to have in six months. Your actual, today budget. Then figure out what's negotiable and what's not.

If you're looking at the numbers and your debt is the real problem — if you owe that R91,000+ like the average South African — then budgeting alone isn't going to move the needle. That's when you might want to compare consolidation options on RandCash or talk through whether debt review makes sense for you. Sometimes the kindest thing you can do for yourself is face what you're actually dealing with and fix the root problem, not just manage the symptoms.

Your budget is a tool. It's supposed to serve you, not stress you. If it's stressing you, change it.