The Phone Call That Changes Everything

It is 9 PM on a Wednesday. Your mother calls — she has been hospitalised and needs R12,000 for a procedure not covered by her medical aid. Or your car, the one you use to get to work every day, dies on the N1 and the mechanic says R8,500 to fix it. Or your daughter is starting university in two weeks and her residence requires a R5,000 deposit by Friday.

These are not theoretical situations. They happen to South African families every single day. And in those moments, many people face a real question: is taking a personal loan actually the right move — or is it digging a deeper hole?

This article gives you an honest framework for thinking through exactly that. Not the sanitised version that tells you debt is always bad, and not the reckless version that says borrow freely. Just a clear-eyed look at when borrowing for an emergency or a family occasion genuinely makes sense, and when it does not.

Part 1: Borrowing for an Emergency

What counts as a real financial emergency?

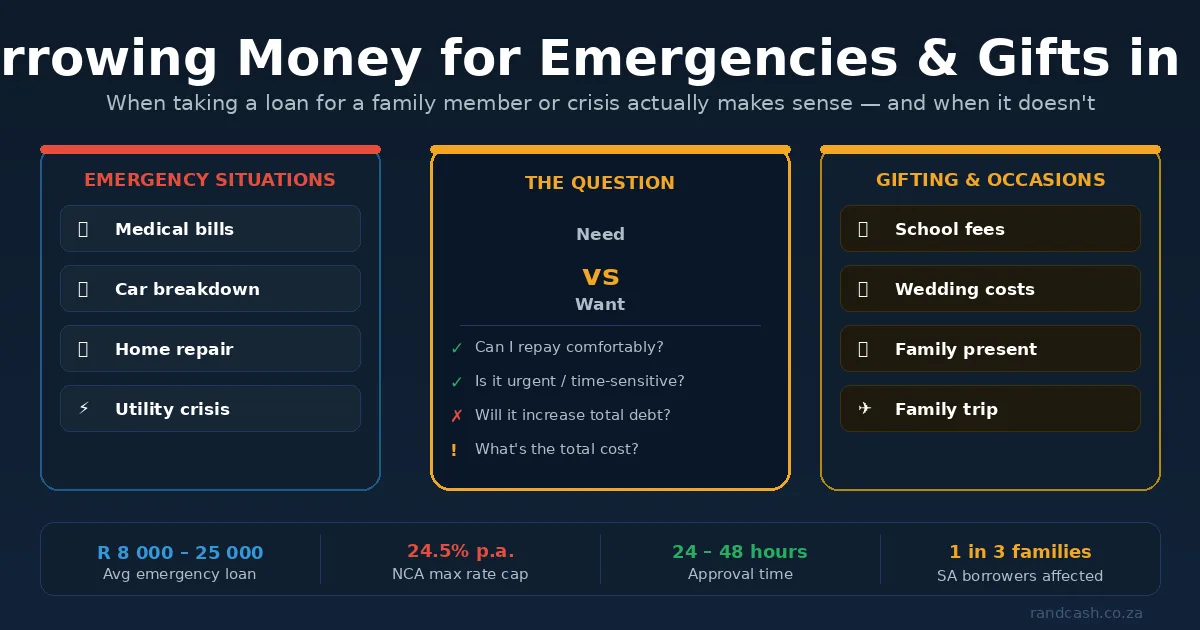

An emergency is something unexpected, time-sensitive, and consequential if left unaddressed. In South Africa, the most common ones that push people toward credit are:

- Medical costs not covered by medical aid or government hospitals — procedures, medications, specialist consultations

- Vehicle breakdowns where the car is essential for work or family care

- Home damage — a burst geyser, a roof leak ahead of the rains, broken security infrastructure

- Job loss or income gap — bridging the period before a new job starts or a settlement pays out

- Death in the family — funeral costs, which in SA can run R15,000 to R40,000 and often fall on families with no funeral policy

Note what is not on that list: a sale at Makro. A concert. A new phone. Those are wants dressed up as needs in the moment. The distinction matters enormously when you are deciding whether to carry debt.

The honest maths of emergency borrowing

Let us say you need R10,000 urgently and you take a personal loan over 12 months at 20% interest — a realistic rate from lenders like African Bank or Capitec for a reasonable credit score.

Your monthly repayment will be approximately R927. Total repaid over 12 months: roughly R11,124. The emergency cost you R1,124 extra in interest — plus about R1,207 in initiation fees (capped under the NCA) and R828 in monthly service fees.

So the real total cost is closer to R13,159. You borrowed R10,000 and it cost you R13,159 to do so.

That sounds alarming. But compare it to the alternative: the vehicle is not repaired, you lose your job, and you lose six months of income. Or the medical procedure is delayed and costs three times as much later. Or the funeral does not happen with dignity and your family carries that weight for years.

Sometimes R3,159 in borrowing costs is the best money you ever spent.

What to check before borrowing for an emergency

Before you apply, run through these honestly:

1. Have I exhausted no-cost options first? Can family lend you the money interest-free? Does your employer offer salary advances? Does your medical aid have a gap cover claim you have not submitted? Is there a SASSA grant you qualify for? Check these first — they cost you nothing or far less.

2. Can I actually repay this comfortably? The NCA requires lenders to do an affordability assessment — but they are looking at whether you can repay, not whether you should. You know your own budget better than they do. If the monthly repayment means you skip groceries or another bill, the loan may solve one problem while creating three more.

3. Am I borrowing the minimum necessary? It is tempting to borrow R15,000 when you need R10,000 — just in case. Resist this. Every extra rand costs you interest and increases the risk that you end up over-indebted.

4. Do I understand the total cost of credit? Every lender is legally required to show you the total cost of credit before you sign. Read it. The monthly instalment figure is not the number that matters — the total repayment is.

Part 2: Borrowing for a Family Gift or Occasion

The different weight of "want" debt

This is where things get more complicated — and more personal. Borrowing to give someone you love a meaningful gift or experience carries emotional logic that pure financial logic sometimes misses.

A grandmother paying for her grandchild's school camp. A father taking a loan to cover his daughter's matric dance dress and photographs. A husband surprising his wife with a trip to Cape Town for their 25th anniversary. Parents who pool savings and a small loan to help their child put down a deposit on a first flat.

Are these reckless? Not necessarily. South African family structures often mean financial obligations flow in multiple directions — upward to parents and grandparents, sideways to siblings, downward to children. Ignoring that reality does not make it disappear.

When it can make sense

Borrowing for a gift or family occasion is more defensible when:

- The occasion is genuinely once-in-a-lifetime or high-stakes — a matric, a wedding, a major milestone

- The amount is modest relative to your income and the repayment term is short (6 to 12 months maximum)

- You are the only realistic way to make this happen — there is no-one else in the family who can contribute

- The emotional cost of not doing it is genuinely significant — not just disappointing, but damaging to relationships or someone's life opportunities

A R5,000 loan over 6 months to cover school registration fees that would otherwise result in your child missing a year of school? That is defensible. A R30,000 loan for a birthday party that the guest of honour would have been equally happy to celebrate quietly at home? That is harder to justify.

The social pressure trap

Here is something nobody writes about directly: in many South African communities, there is real social pressure around funerals, weddings, and milestone celebrations. Expectations around lobola negotiations, tombstone unveilings, and year-end gatherings can push families into debt that takes years to recover from.

This is not a cultural critique — it is a financial reality. And it means the question is not just "can I afford this?" but "am I borrowing because it is the right thing for my family, or because I am afraid of what people will think if I do not?"

Only you can answer that honestly. But it is worth asking before you sign.

The gift loan checklist

If you are considering borrowing for a family occasion or present, ask yourself:

- Is this a need within my family structure, or a want driven by external expectations?

- Will the recipient know about the loan, and do they want you to carry this debt for them?

- Is there a scaled-back version of this that achieves the same emotional outcome at lower cost?

- What happens to my family's financial health if something goes wrong — job loss, illness — while this loan is running?

What Type of Loan Works Best for These Situations?

Not all credit products are equal. Here is how the main options stack up for emergency or occasion borrowing:

Personal loan — Fixed monthly instalments, fixed interest rate, clear end date. Usually the best option for amounts above R5,000 if you have a reasonable credit score. Apply from lenders like African Bank, Capitec, or FNB.

Payday loan — Quick access, but extremely expensive. Only makes sense if you genuinely need money for 2 to 4 weeks and are 100% certain your next salary lands on time. If there is any uncertainty, avoid.

Credit card — If you already have one, using it for an emergency and paying it off within 55 days costs you nothing in interest. Useful tool if you have the discipline. Dangerous if you do not.

Revolving credit facility — Some lenders offer revolving credit that you can draw down and repay repeatedly. Can be useful for recurring family financial support, but the always-available credit line is a temptation risk.

Stokvel advance — If you are part of a stokvel, some groups allow emergency advances to members. Zero interest, community accountability, and you are borrowing from people who know your situation. Underutilised in formal financial advice but widely used in practice.

The One Thing That Makes This Decision Clearer

There is a simple mental test that cuts through the noise: If you could not get a loan, what would actually happen?

If the honest answer is "something genuinely bad — my mother does not get treatment, my car is stuck and I lose my job, my child misses their school registration" — then borrowing is likely justified, provided you can repay it.

If the honest answer is "the party would be smaller" or "the gift would be less impressive" — that is useful information too. It does not automatically mean you should not borrow. But it does mean the decision is about values and priorities, not necessity. And it is worth being clear-eyed about that difference before you sign a credit agreement that will follow you for 12 to 60 months.

After You Borrow: Make It Count

Whether the loan was for an emergency or an occasion, the same rules apply once you have the money:

Use it only for what you borrowed it for. It sounds obvious, but the temptation to use leftover loan money for other things is real and should be resisted entirely.

Set up a debit order immediately. Do not leave the repayment to willpower. Automate it so that the repayment happens before you have the chance to spend the money elsewhere.

Track it on your budget. The loan repayment is now a fixed cost for the next N months. Build your budget around it, not the other way around.

And when it is paid off — do not rush to the next loan. Give yourself a few months to rebuild your buffer. That buffer is what makes the next emergency survivable without credit.

The Bottom Line

Borrowing money for an emergency or a family gift is not inherently irresponsible. What makes it responsible or irresponsible is the decision-making behind it: whether you understand the cost, whether you can genuinely afford the repayments, and whether the thing you are borrowing for is worth what it will actually cost you.

South Africa has one of the highest personal debt burdens in the world. That is partly because credit is accessible. But it is also because many people borrow without running these numbers first. You now have the framework. Use it.