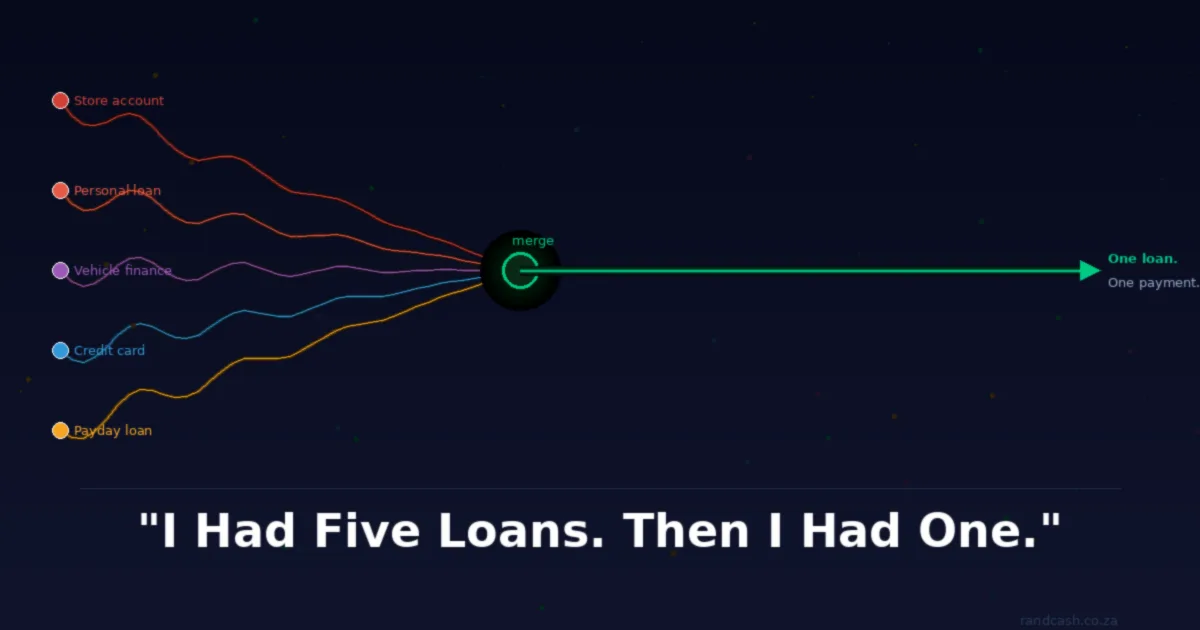

Nandi is 34, a logistics coordinator from Johannesburg. At her worst, she was managing five separate debt repayments every month — a store account, two personal loans, a credit card, and a vehicle finance deal. Last year she consolidated everything into a single loan. We sat down with her to find out how it happened, what it cost her, and what she wishes she had known from the start.

▶ How did you end up with five different loans at the same time?

Honestly? It happened slowly. The first one was a store account — Edgars, back when Edgars was still around. That felt normal, everyone had one. Then I needed a new laptop for work, took a small personal loan. Then my car broke down and I couldn't afford repairs out of pocket, so I used a credit card. Then I needed to sort out a family thing — there was a funeral — and I took another personal loan because the credit card was already sitting at the limit.

None of those individual decisions felt crazy at the time. Each one had a reason. But you don't really see the picture until you're sitting at your kitchen table with a piece of paper listing everything you owe, and the total just sits there looking at you.

▶ What did that picture look like? What was the total monthly payment?

I was paying out about R7,400 a month across everything. My take-home at the time was R18,500. So before I bought groceries, paid rent, put petrol in the car — more than 40% of my salary was already gone. Debt repayments first, living second.

And it wasn't even the amount that broke me. It was the dates. The store account went off on the 1st. The credit card on the 5th. One personal loan on the 15th. The other on the 20th. Vehicle finance on the 25th. I was monitoring my account every few days scared of what was going to hit and when. That kind of vigilance is exhausting. You stop living and start just managing.

▶ When did you first start thinking about consolidation?

I'd heard the word but didn't really understand what it meant. Someone at work mentioned it — she said her cousin had done it and the monthly payment came down a lot. I looked it up and read a few things and then honestly I almost talked myself out of it because I kept reading conflicting things. Some articles said it was a trap. Others said it was the smartest thing you could do. I was confused.

What actually pushed me was missing a payment. Not on purpose — I just lost track. The 15th debit order went off when my account was short because I'd paid for tyres two days before. And the bank charged me R185 in unpaid debit order fees on top of the missed payment. I sat in my car in the parking lot outside Checkers and just thought — I cannot keep doing this. Something has to change.

▶ So what did you actually do? Walk us through the process.

First I wrote everything down. Every account. Every outstanding balance. Every interest rate. Every monthly payment. Every end date. It took me about two hours and I needed a glass of wine after, but I had the full picture for the first time.

Then I started looking for a lender who could give me a single loan large enough to clear all of it. What I was looking for was a rate lower than the average of what I was already paying — some of those store account rates were sitting at 22% to 24%. If I could consolidate into something at 17% or 18%, I'd be paying less interest overall even if the term was longer.

I found a registered lender online, went through their application, they did an affordability assessment, and about two days later I had an offer. The consolidated loan was R62,000 at 18.5%, over 48 months. Monthly payment: R1,850. I went from R7,400 a month across five accounts to R1,850 on one. I nearly cried when I saw it.

▶ That seems like a massive difference. Is there a catch?

Yes — and I want to be honest about this because people need to understand what they're actually doing. The monthly payment was so much lower partly because I stretched the term to 48 months. My previous loans had between 12 and 24 months left on them. So in some cases I was resetting shorter debt back to four years.

That means the total interest I pay over the life of the consolidation loan is not automatically less than what I would have paid on all the individual loans. On a pure numbers basis, you have to do the maths properly. What consolidation gave me was lower monthly pressure, one payment date, and a fixed end point. What it didn't automatically give me was a cheaper loan in terms of total rand paid.

My advice is to ask the lender to show you the total cost of credit over the full term. Not just the monthly payment. Add up what you would have paid finishing your existing loans versus what you'll pay on the consolidated one. Sometimes consolidation wins outright. Sometimes it's a trade — you pay more total but you reduce monthly pressure enough to stop missing payments and getting hit with fees and penalties. Both outcomes can be worth it depending on your situation.

▶ Did you immediately close all the old accounts once you consolidated?

Yes, and this is non-negotiable in my opinion. I used the consolidated loan money to pay off every single account on the same day. Then I closed the store account and the credit card completely. Not just paid them off — closed. Done.

Because here's the trap: some people consolidate and then leave those accounts open with a zero balance. And then life happens, and six months later the credit card has R8,000 on it again. Now they have their consolidation loan payment plus a new credit card balance. That's not refinancing your debt — that's doubling it over time. You have to close the accounts or the whole exercise is pointless.

▶ What does life feel like now, on the other side of it?

I have a savings account now. That's the thing I say when people ask me this question. I have a savings account. R500 a month going in, automatically. It's not a lot. But before consolidation, the concept of saving anything felt like a joke — every rand was already spoken for.

And the mental load is completely different. I used to spend a lot of energy just tracking dates and balances and worrying. That energy is available for other things now. My work has improved. My relationships are better. Stress about money isn't background noise the whole time.

I'm not out of debt. I've still got three years on this loan. But it's manageable debt with a clear end date, and I'm not adding to it. That's a different world from where I was two years ago.

▶ Last question — what would you tell someone sitting where you were two years ago?

Write it all down first. Every single account. Don't estimate — get the actual numbers. Until you see the full picture on paper, you can't make a proper decision. I spent two years avoiding that piece of paper and it cost me.

Then find a lender registered with the NCR — check the registration number, it should be right there on their website. Get the consolidation offer. Read the total cost of credit, not just the monthly. Ask them to explain anything you don't understand. If they won't, find someone else.

And then, if you do it — close the old accounts. All of them. That step is the difference between consolidation fixing your situation and just adding another layer to it.

You're not stupid for having multiple loans. Life is expensive and things happen. But you can get out of it. I did.

If you recognise your situation in Nandi's story, our guide on debt consolidation and refinancing in South Africa walks through how the process works and what to look for in a lender. You can also browse NCR-registered lenders to compare options before you apply for anything.

* Nandi's name has been changed at her request. The financial figures are her own.

— Romans