My accountant thought I was mad.

This was about three years back, sitting in his office in Sandton. I'd just told him I wanted to take a R150,000 personal loan to finance a vehicle I needed for the business. He looked at me over his glasses the way accountants do and said, slowly, "Romans. You have R200,000 sitting in your current account."

I know, I said. I still want the loan.

He actually put his pen down.

Here's the thing most people in Mzansi grow up believing: debt is bad, paying cash is good, and if you have the money to buy something outright then you should absolutely do exactly that. Your gogo told you. Your dad told you. The church probably told you too. Debt equals struggle. Cash equals freedom.

And look — for a huge portion of South Africans dealing with mashonisas, 30%-plus store accounts, and payday loans that eat half a month's salary before you even get home, that framing is completely correct. That debt is destructive. It compounds against you.

But there's another kind of debt. Cheap, structured, NCA-regulated debt from a registered lender. And when you use it right, it doesn't fight you — it works for you.

Let me explain what I mean.

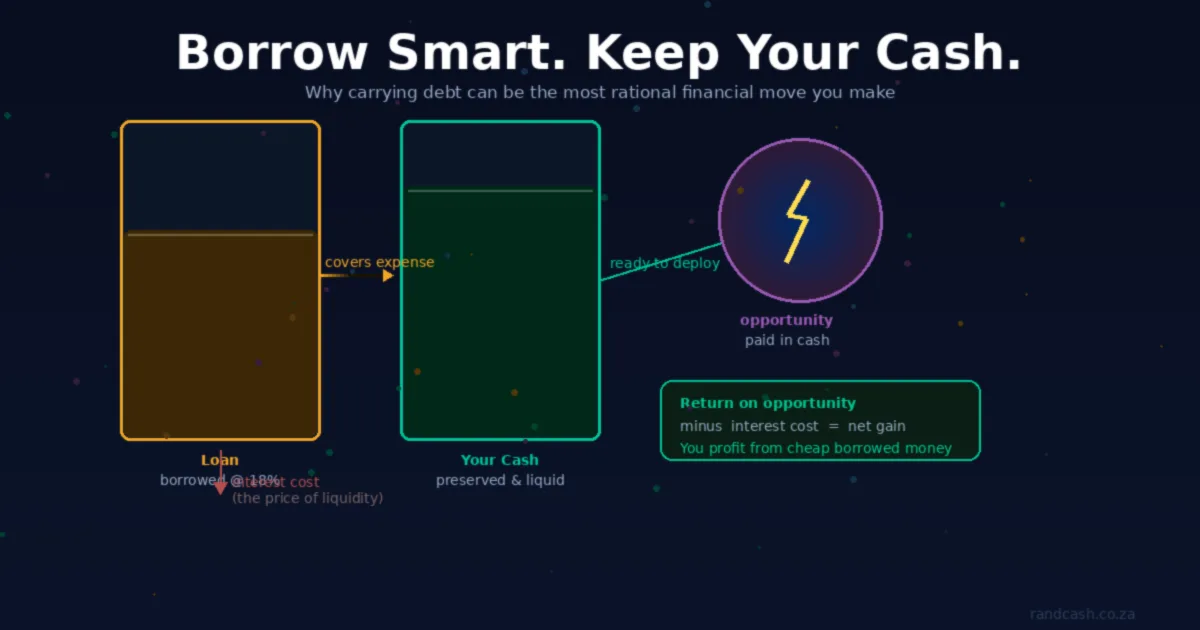

When I took that R150k loan at 16% interest, my monthly repayment was about R3,700 over 48 months. Total interest paid over the life of the loan: roughly R28,000. That's the cost.

The R200,000 I kept in my account? Six months later, a mate of mine in the property game called me. He'd found a small flat in Roodepoort — distressed seller, quick sale, asking R190,000 below market value. Needed to close in ten days.

I bought it. Cash deal. Closed in eight days.

Resold eight months later at R140,000 profit.

Net position after paying off the car loan interest: up R112,000. If I'd paid cash for the bakkie, I'd have had nothing to move with. The opportunity would have walked past me while I stood there with clean hands and an empty account.

That R28,000 in loan interest was the cheapest capital I've ever deployed. It rented me R200,000 in liquidity for four years.

The concept has a fancy name in finance — "opportunity cost of capital." But honestly you don't need the jargon. The simple version is this: your cash has a price. When you spend it, it's gone. When you keep it and borrow instead, you're paying the lender's interest rate to rent their money — and you're betting that your cash will do something more valuable in the meantime.

Sometimes it does. Sometimes it doesn't. That's the honest version.

But here's where Mzansi specifically makes this interesting. We live in a country where deals move fast and windows close faster. The good properties in Joburg and Cape Town get snapped up before they ever hit Property24. The spaza that opens on the right corner in Soweto is gone to someone else the same week. The taxi route that comes up for transfer — you need cash, you need it now, and you need it before the next guy shows up with his.

If your money is all tied up in a paid-off car and a paid-off fridge and a paid-off flat-screen, you're asset-rich and opportunity-poor. Eish. That's a tough position to be in when something lekker lands in front of you.

The load shedding era taught a version of this to a lot of small business owners, actually. The people who moved fastest on solar installations — who negotiated group buys, who bought inverters in bulk and resold them — were the ones with liquid cash when stock was scarce and prices were spiking. The ones who'd spent their savings paying off debt were scrambling. Not because they made bad decisions. Because they'd optimised for zero-debt at the cost of zero-flexibility.

There's a version of this that plays out at every level. A mate in Durban had R80,000 saved for a kitchen renovation. His building contractor mentioned an industrial bakery unit coming up for sale at liquidation price — commercial ovens, mixers, the works — for R65,000. The guy had the money but had mentally ring-fenced it. He let it go. That equipment resold six months later for R140,000. He renovated his kitchen instead.

Not wrong exactly. Just... expensive inaction.

Now — and I want to be straight with you here — this only works if a few things are true.

One: the loan rate has to be genuinely manageable. If you're carrying debt at 28% and your best savings account is paying 8%, the maths is working against you every day you don't pay it off. The concept of "strategic debt" only applies when the interest rate is low enough relative to what your cash can realistically return. In the current environment with prime at 10.25%, a personal loan at 15-17% is expensive — but not prohibitive if your cash is genuinely being put to work.

Two: you actually need to be someone who will keep the cash separate and protected. Not "I'll just use some of it for month-end expenses" separate — genuinely, psychologically, hands-off separate. If you're going to slowly erode that cushion on everyday spending while carrying a loan, you're just paying interest for nothing. That's the trap. The loan becomes the liability without the asset.

Three: the "opportunity" you're holding cash for has to be real. Holding R150,000 in a current account for three years waiting for a deal that never comes, while paying loan interest the whole time — that's not strategy, that's expensive wishful thinking. If your cash sits idle, the loan wins. Pay it off.

My own rule is what I call a "cushion plus trigger" approach, and it's pretty simple. I keep a defined liquid cushion — enough to handle any surprise expense and enough to move on a deal within 48 hours if something comes up. The cushion size depends on what I'm watching. Actively looking at property? Higher cushion. No specific opportunities in view? Lower cushion, redirect cash toward loan repayment.

The point is intentionality. You're not just leaving money in the account because you're scared to use it. You're leaving it there because it's your deployment capital, and it has a job: it's waiting for the right moment.

There's also something nobody talks about enough, which is the psychological value of liquidity.

When you know you have cash available — actual cash, not credit, not an overdraft, not a "I could probably apply for something" — you make better decisions. You negotiate better because you can actually walk away. You don't accept a bad deal on your car trade-in because you're desperate for the cashback. You don't panic-sell an investment during a market dip because you need the cash to cover something else.

Ja, the loan costs you money. But the mental clarity that comes from knowing you're not a single bad month away from a problem? That's real value. It doesn't show up on a spreadsheet. It shows up in the quality of the calls you make.

I'm not saying everyone should run out and take unnecessary debt. I'm saying the framing of "always pay cash if you have it" is simpler than reality.

Sometimes the most financially sophisticated thing you can do is borrow cheap money, keep your own money liquid, and stay ready. In a market like South Africa — unpredictable, fast-moving, full of distressed sellers and random windfalls — optionality has enormous value.

The accountant gets it now, by the way. He's borrowed money to keep cash on hand twice since that conversation.

Sharp.