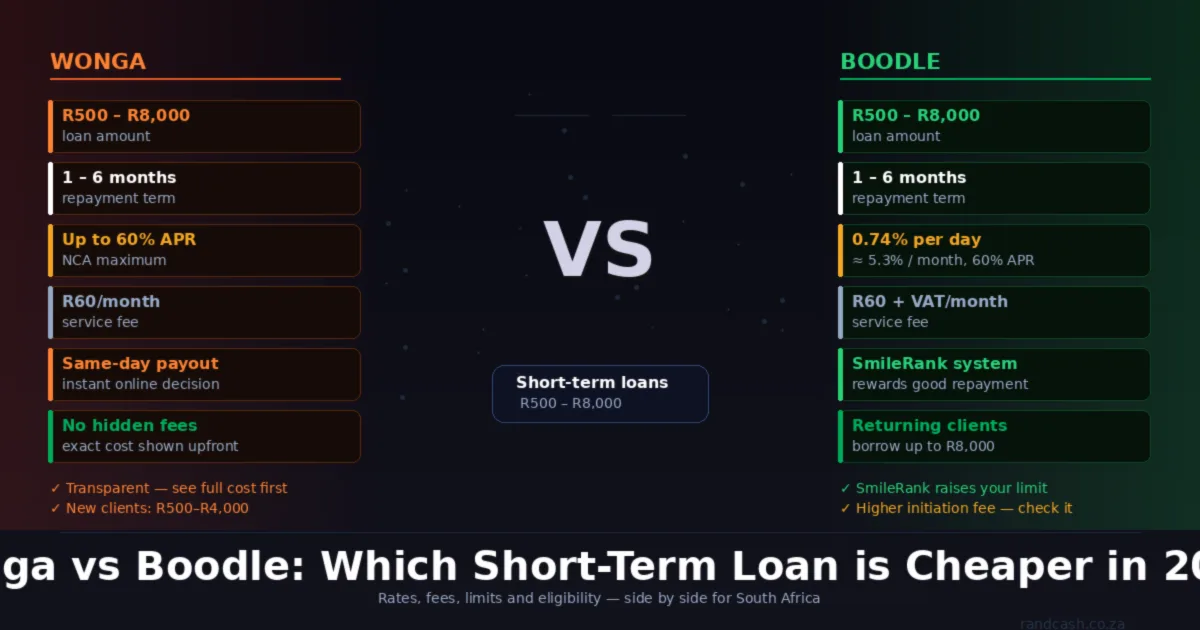

Wonga and Boodle are two of South Africa's most recognised short-term lenders. Both offer small, fast loans — typically between R500 and R8,000 — with decisions in minutes and payouts on the same day. Both are NCR-registered. Both are legitimately used by hundreds of thousands of South Africans when they need cash quickly between paydays.

But they are not the same product. The fee structures differ, the rate calculations work differently, and the cost of borrowing the same amount for the same period can come out to a noticeably different number depending on which one you use. This article shows you exactly how they compare.

| Feature | Wonga | Boodle |

|---|---|---|

| Loan amount (new) | R500 – R4,000 | R500 – R4,000 |

| Loan amount (returning) | Up to R8,000 | Up to R8,000 |

| Repayment term | 1 – 3 months (new), up to 6 (returning) | 1 – 6 months |

| Interest rate | Up to 5% per month (NCA max) | 0.74% per day (≈5.3%/month) |

| Effective APR | Up to 60% | Up to 60% |

| Monthly service fee | R60 | R60 + VAT (≈R69) |

| Initiation fee | R165 or 15% of amount (capped R1,207.50) | R165 + 10% of loan + VAT |

| Loyalty system | Returning client limits | SmileRank (raises your limit) |

| Decision speed | Instant online | Instant online |

| Payout speed | Same day | Same day |

How the fees actually work — a real example

Let's borrow R2,000 for one month from each lender.

Wonga — R2,000 for 30 days:

Interest: 5% × R2,000 = R100

Initiation fee: 15% × R2,000 = R300 (capped at NCA maximum)

Service fee: R60

Total you repay: approximately R2,460 — cost of credit: R460

Boodle — R2,000 for 30 days:

Interest: 0.74% × 30 days × R2,000 = R444

Initiation fee: R165 + (10% × R2,000) + VAT ≈ R389

Service fee: R60 + VAT ≈ R69

Total you repay: approximately R2,902 — cost of credit: R902

On a one-month loan of R2,000, Wonga works out significantly cheaper. The daily interest model at Boodle adds up quickly over shorter periods, and the initiation fee structure is different — Boodle charges VAT on top of the initiation fee, which Wonga doesn't.

The picture changes slightly for longer terms. Over 3 months, Boodle's 0.74% daily rate compounding is worth calculating carefully against Wonga's fixed monthly rate — use whichever lender shows you the full cost breakdown before you confirm.

The SmileRank system (Boodle)

Boodle uses a proprietary scoring system called SmileRank, which tracks your repayment behaviour on Boodle loans. The better your history with them, the higher your SmileRank and the higher the loan limit they will offer you as a returning client. This is similar to how Wonga adjusts limits for returning clients, but Boodle makes the system more explicit and gamified. If you repay consistently and plan to borrow from Boodle multiple times, your access improves over time. If you miss a repayment, your SmileRank drops.

When to use Wonga

Wonga is well suited to borrowers who want price transparency upfront. The Wonga site shows you exactly what you will repay before you confirm — no surprises. For one-month loans in particular, Wonga's fee structure tends to produce a lower total cost than Boodle's. Wonga is also one of the more established short-term lenders in South Africa and has been operating here since 2011. If you need a straightforward payday loan and want to see the full cost before committing, Wonga is a solid starting point.

When to use Boodle

Boodle can work out better for returning clients who have built up a SmileRank, since higher limits become available without a separate application process. If you have an established relationship with Boodle and your repayment history is clean, the convenience of accessing higher limits quickly may outweigh the slightly higher fee structure. Boodle also suits borrowers who prefer dealing with a lender that explicitly rewards loyalty through a structured system rather than informal returning-client upgrades.

Both lenders are legitimate, both are NCR-registered, and both serve a genuine purpose in the short-term credit market. The key is to use either product only for short-term emergencies, not as a recurring income supplement — at 60% APR effective, a R2,000 loan taken monthly adds up to a significant cost of living over a year.

Before borrowing from either, check whether the repayment will leave you short at the end of next month, which is the pattern that drives repeat borrowing. If the answer is yes, a short-term loan is likely to compound rather than solve the problem. In that case, debt counselling or a conversation with a registered credit provider about a longer-term, lower-rate product may be the better route.

See our full list of NCR-registered lenders for more options, or read our guide on every credit type in South Africa compared to understand where short-term loans fit in the broader picture.

— Romans