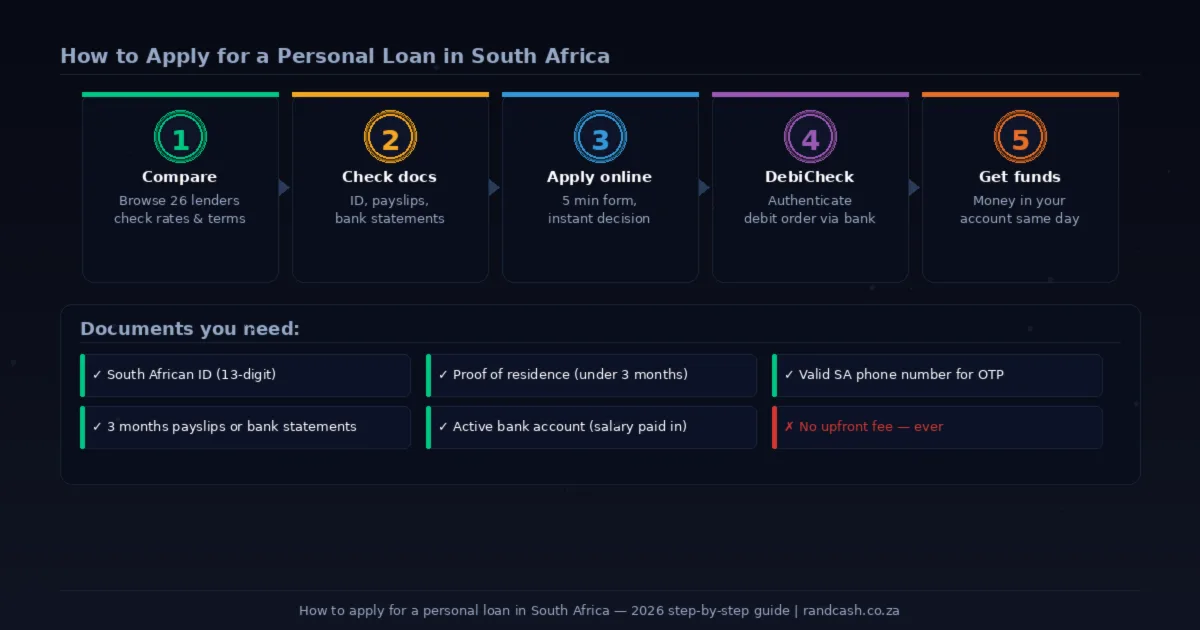

Applying for a personal loan in South Africa takes five to ten minutes online if you have the right documents ready. The process is the same whether you are applying to a bank or an NCR-registered non-bank lender — the legal framework is identical, and every registered lender is required to run the same affordability assessment before approving credit. This guide walks through every step, explains what lenders are actually looking for at each stage, and covers the parts of the process that most other guides leave out — including DebiCheck, which is where first-time applicants most often get stuck.

Step 1: Know what you need before you apply

The fastest applications are the ones where all documents are ready before the form is opened. Gathering these after you start creates delays that can push a same-day decision to the next business day. Here is the standard checklist for a personal loan application in South Africa in 2026:

Required for all applicants: South African ID (green book or smart card, with your 13-digit ID number), an active South African bank account in your name (this must be the account your salary is paid into), your three most recent payslips, your three most recent bank statements showing salary deposits, proof of residence not older than three months (a utility bill, municipal statement, or signed letter from a landlord), and a valid South African cellphone number for OTP verification and contract signing.

If you are self-employed: Replace payslips with six months of business and personal bank statements, plus either a letter from your accountant confirming your monthly drawings, or your most recent tax assessment from SARS. The self-employed application takes longer because income is less predictable — but it is not automatically declined.

Minimum income requirements: Most lenders require a minimum gross monthly income of between R2,500 and R7,500 depending on the institution. Major banks (Absa, FNB, Nedbank, Standard Bank) typically set higher thresholds of R5,000–R7,500. Non-bank lenders like Wonga, Finance27, and Atlas Finance have lower minimums, sometimes from R2,500.

Step 2: Compare lenders before you apply to one

This step is skipped by most first-time borrowers, and it is the most expensive mistake you can make. The interest rate you receive is personalised — it will differ between lenders based on how each institution scores your profile against their internal risk model. Applying to the first lender you find and accepting whatever rate they quote is almost never optimal.

The comparison criteria that matter most are: the interest rate (APR, not just the monthly rate), the initiation fee (capped at R1,207.50 by the NCA, but some lenders charge less), the monthly service fee (capped at R69 by the NCA), the total cost of credit over the full term, and whether the lender is NCR-registered.

Most lenders offer a quote online before you formally apply. A quote typically involves a soft credit check, which does not affect your credit score. Use this to get comparable figures from two or three lenders before committing. RandCash lists all 26 NCR-registered lenders on one page for exactly this purpose.

Step 3: Complete the application form

Once you have selected a lender, the online application form typically takes five to ten minutes. You will be asked for: personal details (name, ID number, date of birth), contact details (phone, email, address matching your proof of residence), employment details (employer name, employment start date, salary date), financial details (gross monthly income, existing monthly debt repayments), and banking details (bank name, account number, branch code).

Some lenders use Open Banking to pull your bank statements directly from your bank with your permission, removing the need to upload documents manually. FASTA is the most prominent example — for Capitec clients, this reduces the application to under five minutes with no document upload required. Where Open Banking is available, use it: it speeds up the decision and reduces the chance of data entry errors.

Be accurate. Lenders verify every figure you provide against your bank statements and bureau data. Discrepancies between what you declare and what the statements show trigger manual review, which delays the decision.

Step 4: The affordability assessment

Every NCR-registered lender in South Africa is legally required under the National Credit Act to conduct a formal affordability assessment before approving your application. This is not optional, and a lender who skips it is operating illegally. The assessment calculates whether you can realistically repay the proposed loan without being placed under undue financial stress.

The calculation: gross monthly income, minus tax and deductions, minus existing monthly debt repayments, minus estimated basic living expenses (food, transport, utilities), gives your available monthly surplus. The proposed new repayment must fit within this surplus. If it does not, the application will be declined regardless of your credit score.

The most common reason for declining applicants with good credit scores in 2026 is over-commitment — too many existing repayments relative to income. If you are declined on this basis, it is not necessarily a permanent block: paying down an existing credit card or loan before reapplying can change the outcome.

Step 5: Understanding DebiCheck — the step most guides skip

If your application is approved, you will need to sign your loan agreement electronically and authenticate a DebiCheck debit order before funds are released. This step confuses many first-time applicants and delays same-day payouts when it is not completed promptly.

DebiCheck is a South African Reserve Bank-mandated system that requires you to pre-authorise your debit order directly through your bank — not just with the lender. When you accept a loan, your bank sends you a notification (USSD on your phone, or a push notification from your banking app) asking you to confirm the debit order details: the lender name, the amount, the payment date, and the frequency. You must confirm this within the same business day for same-day payout. If you miss the DebiCheck confirmation, payout is deferred to the next business day.

Check your phone immediately after signing your loan agreement. The DebiCheck request comes from your bank, not the lender — some applicants miss it because they are waiting for a message from the lender instead.

Step 6: Funds disbursement

After DebiCheck is authenticated and the loan agreement is signed, funds are transferred to your bank account. For lenders like FASTA, this can happen in under five minutes for Capitec clients. For most other online lenders, expect one to four hours if you have completed the process before 14:00 SAST on a business day. Applications completed after 14:00 typically pay out the next business day.

Repayments are collected by debit order on the date specified in your agreement, usually the date your salary is paid. Ensure your account has sufficient funds on that date. A returned debit order generates a bank charge (typically R120–R155 depending on your bank), a debit order dishonour fee from the lender, and a missed payment on your credit record. Three missed payments in a row triggers adverse listing with the credit bureaus.

What to do if you are declined

A declined application is not a ban. Lenders are required by law to tell you the reason for the decline — request this in writing if it is not automatically provided. Common reasons: insufficient income for the requested amount (apply for less), existing debt commitments too high (pay down before reapplying), negative listings on your credit record (dispute any errors, or apply to a lender with a more flexible credit policy), or employment tenure too short (some lenders require three to six months in a current role).

Do not submit a second application immediately after a decline. Hard inquiries lower your credit score slightly, and multiple applications in quick succession are flagged by lenders as high-risk behaviour. Wait at least 30 days before reapplying, and address the underlying reason for the decline in the interim.

Use our lender comparison page to see all 26 NCR-registered lenders with their amounts, terms and rates. If your credit score is the issue, read our guide on loans for bad credit in South Africa. Need the money today? See our same-day loan comparison.

— Romans